Request a copy of our book(s)

Request a copy of our book(s)Financial Literacy Is Fading with Age

Here’s What the Research Shows—and Why It Matters to Everyone

We all expect to slow down a little as we age. But what if part of what slows down is our ability to understand money?

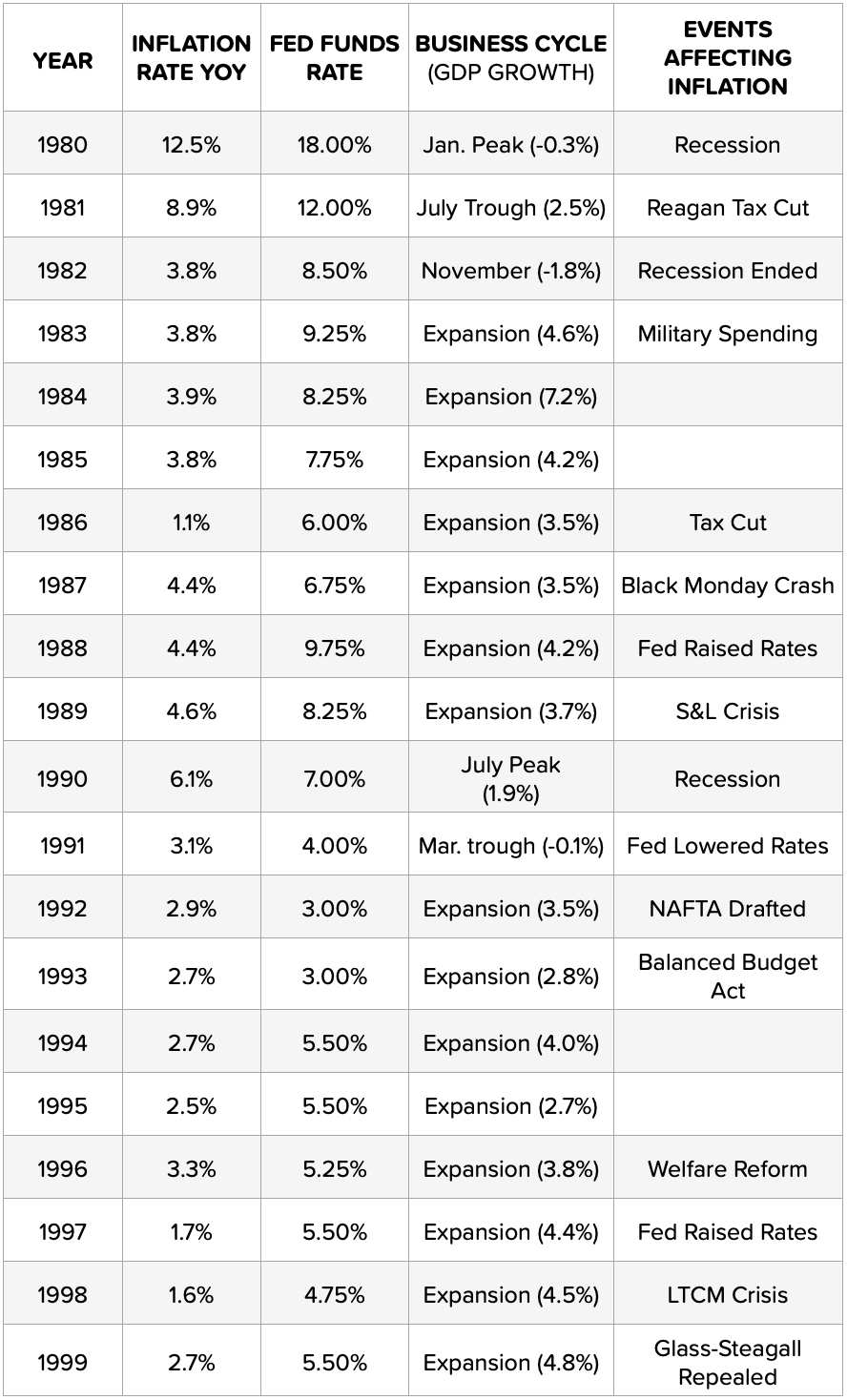

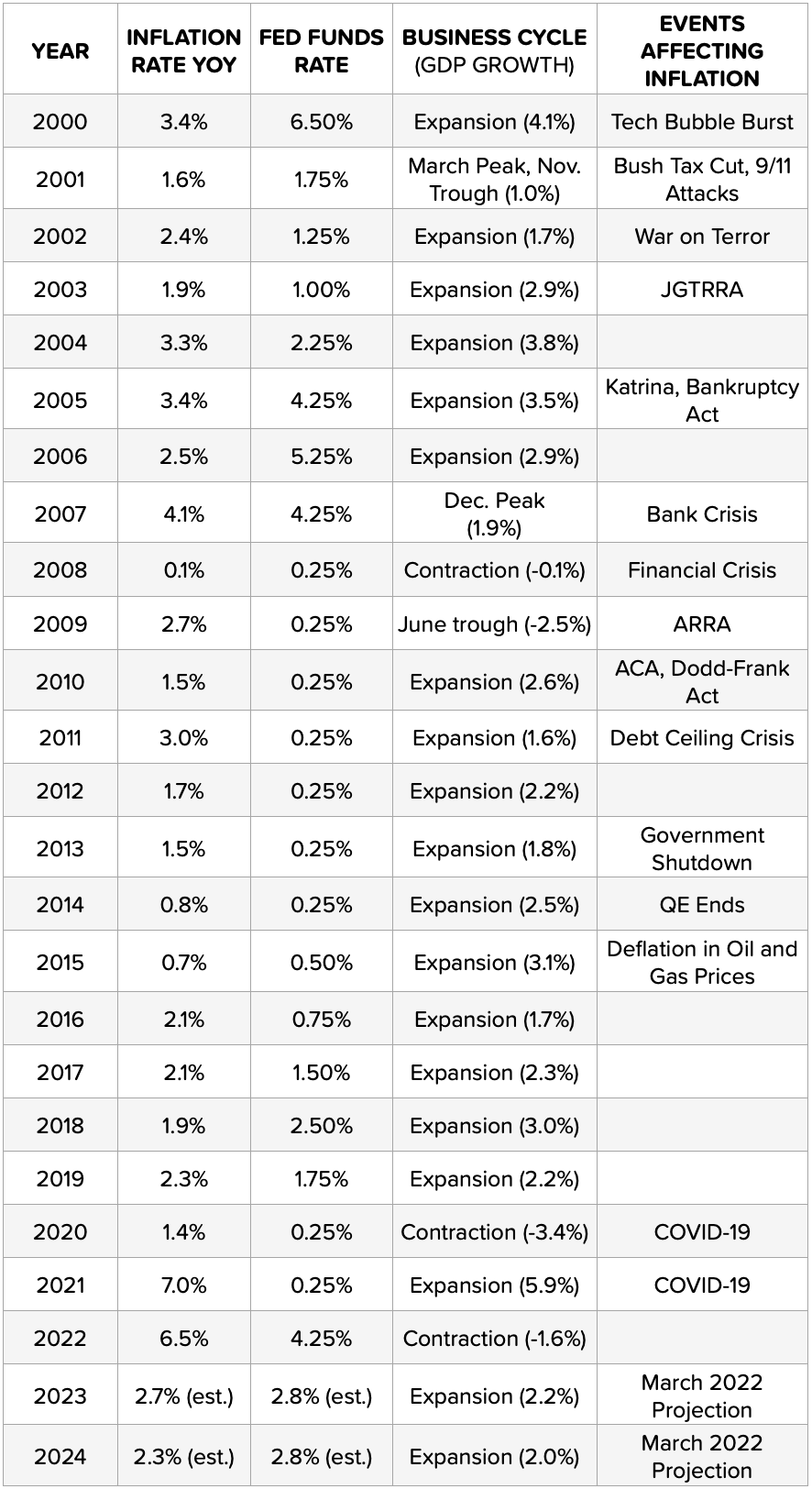

That’s exactly what a groundbreaking study from researchers at Wharton and Rush University Medical Center just confirmed: financial literacy tends to decline with age, and that decline can quietly erode a person’s independence, wealth, and decision-making confidence in retirement.

If you think this only affects people over 80, think again. This isn’t just a retirement issue—it’s a life planning issue. And the earlier we understand what’s at stake, the better equipped we’ll be to face it.

The Big Question: Does Financial Literacy Decline With Age?

Yes. And the data is clear.

The study followed 1,075 adults aged 60 and up (average age 81) over an average of six years, with some participants being followed for up to 13 years, researchers found that:

- Financial and health literacy scores dropped about 1% per year.

- Men started off with higher financial literacy scores than women—by about 9 percentage points—but both genders declined at similar rates.

- Health literacy dropped slightly faster than financial literacy.

- Only 13% of participants avoided any decline at all—the vast majority saw their understanding fade gradually over time.

This decline happened across income levels, education levels, and even among people without dementia. In other words, this isn’t about memory loss or disease—it’s a natural result of aging.

Why This Matters More Than Ever

Let’s zoom in for a second on why this should matter to everyone—especially those in their 40s, 50s, and 60s.

As we age, our financial decisions get more important—not less.

Think about the choices older adults face:

- When to claim Social Security

- Whether to take a lump sum or annuity

- How to manage required minimum distributions (RMDs)

- How to avoid scams and fraud

- Which Medicare or long-term care plan is best

These aren’t just “money” decisions. They’re life decisions. And they often come at a time when we may no longer be at our best financially.

Women Face an Even Greater Risk

While both men and women decline at similar rates, the study revealed that women started at a disadvantage.

They had lower financial literacy scores to begin with, even though they lived longer. And that combination—less knowledge, longer life—can be dangerous.

Many women outlive their spouses and then become responsible for managing retirement income, investments, and estate issues on their own—often for the first time. Without a strong foundation of financial literacy, this can feel overwhelming or lead to costly mistakes.

Health Literacy Matters Too

This study didn’t just measure financial knowledge—it also looked at health literacy. And the results are just as important.

Health literacy is your ability to understand things like:

- Prescription instructions

- Medicare benefits

- Insurance coverage

- Risk information from doctors

- End-of-life care decisions

Just like with finances, health literacy declines over time. And just like with finances, those declines make you more vulnerable—to confusion, bad decisions, or unnecessary hardship.

What’s Causing the Decline?

Researchers don’t pinpoint a single cause, but they do suggest some likely culprits:

- Cognitive aging – Natural changes in brain function can affect how we process numbers, terms, and risk.

- Less financial engagement – Retirement often leads to a “set it and forget it” mindset, reducing the need to actively manage money.

- Stress, illness, and loss – Life’s challenges can make decision-making harder, especially with complex topics.

Importantly, this decline can happen even to people who were once financially savvy. It’s not about intelligence. It’s about how age slowly changes the way we take in and act on information.

So What Can We Do About It?

That’s the good news: there are things we can do—starting today.

Here are six practical steps that can help you protect your future self (or help someone you love do the same):

1. Build Your Financial Literacy Now

The earlier you learn how money works, the longer you’ll benefit. Whether you’re 35 or 65, get educated and stay sharp. Use books, videos, quizzes, or one-on-one conversations with a financial professional.

2. Simplify Your Finances

As you age, simplicity is power. Consolidate accounts. Create clear plans. Make your financial picture easier to manage—not harder.

3. Set Up Trusted Contacts

Most investment firms now allow you to name a “trusted contact”—someone they can call if something seems off. It’s a smart layer of protection.

4. Create a Decision-Making Framework

Use checklists or written guides to walk through important decisions. These tools can help reduce errors later when your energy—or clarity—is lower.

5. Engage Your Spouse or Family

Don’t go it alone. If one partner handles all the finances, make sure both are up to speed. If you have adult children, include them in high-level plans.

6. Work with a Financial Professional

An experienced, trusted financial educator or professional can help you navigate decisions, explain your options, and keep your plan on track—even when life gets complicated.

Final Thoughts: Plan Now, Benefit Later

The study confirms what many people experience firsthand: the older we get, the more we need help understanding the financial world around us.

But this doesn’t have to be a crisis.

It can be a chance.

A chance to:

- Build up your financial literacy before you need it most

- Create systems that protect your future self

- Make decisions today that will serve you for decades

- Help the people you love—parents, grandparents, friends—do the same

Financial literacy may fade with age. But with the right tools, guidance, and planning, your confidence doesn’t have to.

Let’s stay sharp. Let’s stay prepared. Let’s teach the next generation how money works—before the moment they really need it.

Ready to start? Take the Financial Literacy Quiz, talk with a financial professional, or explore TheMoneyBooks Series to begin your journey today.

Because the truth is, financial literacy is a lifelong journey. And while it may get harder with age, that just means we need to be more intentional—more prepared.

How To Stay Smart, Calm, and in Control in Volatile Times

“Should I sell and pull out?”

If you’ve asked yourself that question lately, you’re not alone. Market volatility can feel like riding a financial rollercoaster—complete with gut-turning drops, unexpected turns, and maybe even a scream or two.

But here’s the thing: volatility isn’t the enemy. Ignorance is. And when you learn how money works, you stop being a sucker for fear, panic, and guesswork—and start being a strategist who uses the ups and downs of the market to build wealth over time.

Let’s explore some timeless strategies for navigating uncertain markets, and how connecting with a financial professional can help you turn chaos into clarity.

1. Diversify Isn’t Just a Buzzword—It’s a Buffer

Imagine this: you’re carrying all your eggs in one basket. Then someone bumps into you. Result? Mess everywhere.

The same can happen when you put all your money into one company, industry, or asset type. A single market event could have a big impact on your overall finances.

That’s where diversification comes in. By spreading your investments across a variety of asset classes, you can help reduce risk and create potential for more stable returns over time.

📈 Equities may perform well in a strong economy.

📉 During downturns, fixed income investments can often provide a cushion against volatility.

A balanced approach can help minimize the extreme ups and downs of the market.

Need help creating a diversified strategy that makes sense for you? That’s where a financial professional can guide you, offering solutions tailored to your unique situation.

2. Look for Deals, Not Drama

"Most of us love a good deal. Black Friday? Great discounts. A sale on sneakers? Hard to resist. But when markets drop and investments are priced lower, it’s common to feel uneasy instead of excited.

Market volatility can bring opportunities for those focused on the long term. Think of it like shopping for quality items at a discount. Lower prices may allow you to purchase more shares, which could potentially enhance growth over time.

🛒 You wouldn’t turn down your favorite item just because it’s on sale. The same mindset can often apply to investing.

💡 Warren Buffett’s wisdom offers perspective here: “Be fearful when others are greedy, and greedy when others are fearful.” Instead of reacting with hesitation, times like these might call for a plan.

However, not all discounted investments are created equal. It’s important to know the difference between a solid opportunity and a risky move. Your financial professional can provide guidance tailored to your goals, helping you make informed decisions during uncertain times.

3. Play the Long Game (Seriously, Stay in the Game)

Here’s the truth: constantly checking your investments can lead to stress and impulsive decisions.

Market ups and downs are part of the investing experience. While downturns (bear markets) can be unsettling, history shows they tend to last around 9 months. On the other hand, periods of growth (bull markets) often span several years.

Pulling money out during a dip can lock in losses, whereas staying invested may give your portfolio the chance to recover over time.

📊 Data suggests that missing just a few of the best-performing days in the market over a decade can significantly impact your returns. Interestingly, those standout days often occur amidst tough times.

Navigating market uncertainty isn’t easy. That’s where a financial professional can guide you. They can help create a personalized plan based on your goals, keeping emotions and headlines from steering your decisions.

4. Use This Time to Check In (Not Check Out)

A market downturn offers an opportunity to check in on your financial strategy. Consider asking yourself these key questions:

Are your investments aligned with your short-, mid-, and long-term goals?

Do you have an emergency fund to help avoid tapping into investments during challenging times?

Is your portfolio diversified across different asset classes?

Have you reviewed your risk tolerance recently?

This isn’t about trying to predict market movements. It’s about refining your overall approach and making thoughtful adjustments to stay on track.

If you don’t currently have a clear strategy, now could be the time to build one. A financial professional can guide you in organizing your financial life and help you create a plan tailored to your specific goals.

5. Compound Interest Doesn’t Care About Volatility

Compound interest might just be one of the most valuable tools in wealth building. What makes it remarkable? It doesn’t react to headlines, market swings, or economic predictions. Instead, it thrives on consistency and time.

The earlier you start investing and the more you stay committed, the greater the impact compound interest can have on your financial growth. Even during market downturns, keeping your investments on track allows compound interest to keep doing its job.

Here’s an example to consider:

Investing $200 a month at age 25. If your investments earn an average annual return of 9%, by the time you turn 67, your total investment will have grown to an astonishing $1,125,400.

If you delay and start investing at 35, with the same $200 a month and 9% return, your savings would grow to $443,300 by age 67.

The key takeaway? Volatility is often short-lived, but the benefits of compound growth can build over a lifetime. Staying focused on the long game matters.

Curious about how to put compound interest to work for your future? A financial professional can help you create a strategy tailored to your goals and timeline.

6. Smart Investors Don’t Go It Alone

You don’t have to tackle everything on your own. Many confident investors start by learning the basics and then teaming up with a financial professional to help guide the way.

Think of a financial professional as your financial navigator. They can assist you in staying focused on your goals, adapting to unexpected changes, and creating a plan to reach your destination.

Here’s how they can support you:

- Provide clarity on how market fluctuations impact your goals

- Help design a diversified portfolio tailored to your needs

- Offer guidance on when to adjust your approach, whether it’s buying, selling, or staying the course

- Assist with planning for big milestones like retirement, college, or building an emergency fund

- Help you avoid making emotional decisions that could impact your long-term progress

Just like coaching in fitness or business, having an expert on your side can make a significant difference. You’re still in control—but they provide the tools and guidance to help you move strategically toward your financial goals.

Final Thoughts: The Market Isn’t the Problem—Your Mindset Might Be

Volatility can feel unsettling—we won’t deny that. But if you’re still reading, you’re already taking a step that many overlook: you’re learning.

When you ask thoughtful questions and start exploring how money works, the uncertainty begins to fade. What was once intimidating can start to look like opportunity instead.

The basics are key:

- Understand how money work

- Invest with intention

- Stay committed to your plan

And most importantly? Seek guidance when you need it.

A financial professional can help create a personalized strategy so you can approach the future with clarity and confidence.

Your next move could be the one that changes everything.

Money Doesn’t Care About Gender, But Life Does

Practical Financial Empowerment for Women

As the co-author of HowMoneyWorks for Women and a certified financial educator, I’ve spent years helping people understand how to take control of their finances. If there’s one thing I’ve learned, it’s this: money itself doesn’t care who you are. A dollar doesn’t have preferences, and financial systems operate the same, regardless of gender. But here’s the hard truth—life tends to deal women a unique set of challenges and opportunities, which explains why many of us approach money differently.

From pay gaps to caregiving responsibilities to longer lifespans and more health issues, we tend to start behind and sacrifice more financially. These are not just statistics to me; they are struggles I’ve seen firsthand—with friends, clients, and even in my own life. That’s why I’m passionate about helping more women feel confident about creating, growing, and managing their money. I want to share some practical insights to help you on your own financial path.

Why Women Need to Lead Their Financial Lives

Taking control of your finances isn’t optional for women. With the gender pay disparity, we start from behind. If we don’t take charge of our financial lives, we may fall farther behind, especially if we are raising children or caring for aging parents or other loved ones. Whether it’s retirement savings, emergency funds, or just the confidence to make smart money decisions, the gaps become glaring. Don’t worry if that sounds like you right now. What matters is that you’re ready to start.

For me, that sense of urgency comes from seeing too many women wait until a crisis forces them to figure out their financial situation. My mission is to change that narrative—to help women feel empowered well before they face those moments.

Why Don’t We Talk About Money?

Have you noticed how money usually feels like a taboo topic? It’s not something we openly talk about with friends, family, or even our partners. I grew up believing it wasn’t polite to talk about income or spending. But here’s the thing I’ve learned over the years—that silence hurts us.

Talking about money is an effective way to help us learn, grow, and get stronger. I always encourage women to have those conversations. Sit down with your partner, your family, your friends, or even a financial professional. When you talk about money, it stops feeling scary. You see that you’re not alone – many people share similar fears, frustrations, and dreams for a better future. And, discussing what’s important to us or what’s bothering us helps us clarify what we want and what we need to do. I know this from personal experience and from the women I’ve worked with who felt a shift simply by breaking the silence.

The Power of Knowing Your Numbers

Here’s a tip I share with nearly everyone I work with: Know your numbers. No more guessing or assuming. I mean really understand what’s happening with your money.

What does that look like? For me, it means keeping track of five key areas. You should know:

- How much money is coming in? This could be your paycheck, freelance work, business profits, or passive income streams. Every dollar counts.

- How much is going out? Start paying attention to where your money goes each month. Bills, groceries, subscriptions, shopping, coffee runs... all of it.

- What do you owe? Make a list of all your debts, from credit cards to student loans – what’s the balance and interest rate and how long will it take to pay the debt off.

- What insurance do you have? This is one people often overlook. Check what’s actually covered under your policies and how much are you paying so there are no surprises later.

- What will you need for the future? Whether it’s saving for retirement, buying a home, or your child’s education, start developing a plan for reaching these goals.

When I started tracking my own numbers more closely, it was such a game changer. You can’t make good decisions without information, and this is where it all begins.

Stop Living Paycheck to Paycheck

78% of Americans live paycheck to paycheck.* That’s an overwhelming number of people who are just getting by, with little opportunity to think about their future.

A lot of the women I meet say, “Kim, I can barely get through this week. How am I supposed to save for retirement?” I get it. I’ve been there, too. A common misconception is that you need a lot of money in order to set money aside for the future. Saving and investing for the future is really about taking small, intentional steps on a consistent basis. Saving $1 or $5 or $10 a day, every day, is a step you can take now. All you need to do is start.

What are the most important things you want in your future? Maybe it’s a retirement beyond what social security may provide. Maybe it’s your kids’ college education or saving for a big exotic vacation or just paying off debt. Whatever it is, identify it, claim it, then manifest it by working backward step by step.

Trim Expenses That Don’t Serve You

One simple but powerful thing you can do right now? Go through your expenses and cut out anything that doesn’t add value to your life. Truthfully, I had to do this myself not long ago. After the pandemic, I realized I had subscriptions for several streaming platforms I no longer used or wanted.

It doesn’t seem like much at first, but those little things add up fast. A $10 subscription here and a $30 membership there can mean hundreds of dollars every year you could redirect toward savings or debt. Sit down with your most recent bank account statement and ask yourself, “Do I still need this?”

Inflation and the Need for Smarter Choices

Inflation is making things tougher for all of us. Groceries cost more. Gas costs more. Everything feels like it’s inching beyond reach. On top of higher prices, persistent high inflation translates into higher interest rates on mortgage loans and credit card debt. It’s a double whammy to our pocketbooks. That’s why financial education is even more important right now.

When you understand money, you can maximize what you have—even in tough economic times. I’ve seen women turn their finances around simply by being more strategic about spending, saving, and planning. It doesn’t happen overnight, but it is possible.

My Takeaways for Women

I hope some of what I’ve shared here resonates with you. My message is simple but comes from years of working with women and walking my own financial path. These four actions can transform your relationship with money:

- Talk about money. Seriously, just start the conversation—even if it feels uncomfortable.

- Know your numbers. Information is power.

- Cut back on things that don’t serve you. Free yourself from unnecessary spending to redirect funds toward what really matters to you.

- Plan for the future. No matter how overwhelmed you feel in the short term, think about where you want to be.

Money doesn’t have to be overwhelming or intimidating. You can do this!

It’s Time to Take Charge

If you’ve read this far, it means you’re ready to make a change. And that’s amazing! Financial empowerment starts with small decisions that build over time. Whether it’s cutting an unnecessary subscription, opening a savings account, or reaching out for professional advice, what matters most is that you start.

If you’re ready to learn more, consider reading HowMoneyWorks for Women. It’s packed with insights and practical tips to guide you toward financial independence.

Remember, money might not care about who you are, but your financial future absolutely does. Take control of it. The best time to start is now.

— Kim Scouller

* Forbes, “Living Paycheck to Paycheck Statistics 2024,” Emily Batdorf (Apr 2, 2024). https://www.forbes.com/advisor/banking/living-paycheck-to-paycheck-statistics-2024/

The Role of Women in the Great Wealth Transfer

We live in an extraordinary time for women and wealth. A recent report from Cerulli Associates estimates that over the next few decades, an unprecedented $124 trillion in wealth will transfer from Baby Boomers to their heirs, charities, and spouses, marking one of the greatest financial redistributions in history. Among this massive shift, approximately $40 trillion will flow directly to widowed women, placing them at the center of this economic transformation.

This moment, known as the Great Wealth Transfer, is more than just a redistribution of finances. It’s an opportunity for women to step into economic power, redefine financial independence, and create legacies that align with their personal values. However, it also comes with challenges and crucial decisions that require preparation and a proactive approach.

Insights from our book, How Money Works for Women: Take Control or Lose It, serve as an important tool during this time, offering strategies to address these challenges and inspire women to take control of their financial futures.

Why the Great Wealth Transfer Is a Turning Point for Women

For decades, women have traditionally played secondary roles in financial management, often leaving investments, estate planning, and major financial decisions to their partners. While this dynamic is evolving, societal expectations and systemic barriers have contributed to gaps in financial literacy and economic confidence among women.

The Great Wealth Transfer offers a unique opportunity to break those patterns. With $40 trillion set to transfer to widowed women alone, many will find themselves managing significant assets for the first time. Whether it’s deciding how best to preserve wealth, invest with intention, or support future generations, this newfound responsibility can feel overwhelming.

But it doesn’t have to be. With the right tools, mindset, and support, women can take ownership of their financial destinies and turn this monumental shift into a pathway for empowerment.

Challenges Women Face During Wealth Transfers

While this period represents an opportunity to build financial independence, it’s equally important to recognize the challenges that women may face as wealth recipients and managers.

1. Navigating Emotional and Financial Complexities

Wealth transfers often occur during times of great loss, such as the death of a spouse. Managing financial transitions while navigating grief is nothing short of daunting, especially if finances were not previously a primary focus.

Taking time to process emotions is essential, but so is ensuring financial decisions are approached with care and clarity. Women in this position should seek support from trusted advisors or professionals to help manage the immediate complexities while planning long-term strategies.

2. Knowledge Gaps in Financial Literacy

Many women inherit wealth without prior experience handling investments, taxes, or estate matters. Studies consistently show gaps in financial literacy between men and women, often as a result of traditional household dynamics or societal norms that discourage women from engaging in financial education.

Bridging this gap requires a proactive approach to learning. Empowerment begins with understanding the basics of personal finance, from differentiating between stocks and bonds to knowing the importance of diversifying investments.

3. Overcoming Stereotypes and Expectations

Society has long placed pressure on women to focus their wealth on caregiving or family obligations rather than personal aspirations or long-term financial goals. While supporting loved ones is undoubtedly noble, it’s not the sole purpose of financial resources.

Breaking free from these expectations enables women to wield their wealth in ways that also ensure their security, develop independence, and drive meaningful social impact. Women must give themselves permission to prioritize their own financial health and the goals that matter most to them.

Practical Steps to Take Control of Your Wealth

While challenges remain, the tools for success are well within reach. Here are practical strategies women can use to manage, preserve, and grow their wealth during the Great Wealth Transfer.

1. Educate Yourself and Take an Active Role

One of the first and most empowering steps is to gain knowledge about your finances. This includes understanding existing assets (investments, savings accounts, and real estate), liabilities (debts or loans), and any major estate plans or taxes tied to your inheritance.

Investing in financial education doesn’t have to be overwhelming. Start small by learning the basics of trusts, estate planning, investment strategies, and budgeting. If finance feels intimidating, seek resources specifically tailored to women, such as our How Money Works for Women book, which makes financial concepts accessible and actionable.

2. Choose Advice That Align With Your Vision

Navigating significant financial responsibilities is not something you have to do alone. Building a team of trusted professionals can make all the difference. Seek a financial professional who understands your unique needs and listens to your concerns, rather than taking a one-size-fits-all approach.

The good ones will communicate clearly, help you clarify your goals, and empower you to make informed decisions. Ask questions during consultations and don’t be afraid to interview multiple candidates until you find someone who aligns with your priorities for yourself, your family, and your values.

3. Clarify Your Financial Priorities

It’s important to think about what you want to achieve with your wealth. Some women may prioritize creating a financial safety net, while others may focus on legacy-building through philanthropy or investing in family businesses. Whatever your goals, defining your priorities will help guide your decision-making.

Consider factors like retirement planning, children’s education, charitable contributions, and personal pursuits. By outlining your vision, you create a framework that ensures your wealth works for you—not the other way around.

4. Update or Draft an Estate Plan

If you’ve inherited significant assets, or are managing finances solo for the first time, creating or updating your estate plan is crucial. A comprehensive estate plan ensures that your wealth is distributed according to your wishes and helps avoid unnecessary complications for future heirs.

Tools like trusts or donor-advised funds can also help minimize tax liabilities while supporting your long-term goals. Whether you plan to distribute wealth among your family, invest in philanthropy, or both, having these plans in place will grant you greater control and peace of mind.

5. Align Your Wealth With Your Values

One of the most fulfilling aspects of managing wealth is the ability to align your money with your beliefs. You may want to contribute to environmental initiatives, support women-owned businesses, or give back to underserved communities.

Impact investing, which focuses on social or environmental returns alongside financial ones, is becoming increasingly popular among female investors. Taking this approach allows you to make your wealth not just a tool of personal and family security, but also a driver of social good.

6. Build a Financial Legacy

Beyond immediate needs and goals, think about the legacy you want to leave for future generations. For example, creating educational funds for your children or grandchildren ensures lasting support for loved ones, while contributing to charitable causes allows you to give back to your community in meaningful ways.

Remember, your legacy is not just about the money you leave behind but also the values and priorities you demonstrate through your financial choices. Taking control of your finances now ensures your wealth will reflect the principles that matter most to you.

Trust Yourself and Take Control

The role of women in the Great Wealth Transfer is more than just passive receivership. It’s about becoming informed, making intentional decisions, and taking ownership of the financial opportunities and responsibilities that come your way.

As emphasized in our book How Money Works for Women, education and empowerment are key to navigating this period of change successfully. By taking deliberate steps to educate yourself, align your resources with your goals, and build a trusted support network, you can transform this monumental transition into a moment of empowerment.

The wealth is real; the opportunity is unparalleled. You have the tools and capabilities to make impactful choices that protect your future, enhance your independence, and leave a legacy as bold as you are. This era is a testament to what women can achieve when they take control of their financial destinies. Go forward confidently, and own your story.

Household Debt is Growing at Alarming Levels

And How We Can Turn It Around

Debt has become a staple of modern life. Most people rely on loans or credit cards for significant purchases like homes, education, or emergencies. However, there’s a fine line between productive debt and a dangerous spiral of financial instability. Right now, household debt is edging closer to the danger zone.

According to the 2024 Q4 Household Debt and Credit Report from the Federal Reserve Bank of New York, household debt has reached a staggering $18.04 trillion—that’s a $93 billion climb in just three months. Credit card balances alone have skyrocketed by $45 billion, marking a concerning 7.3% increase from the previous year and bringing the total to $1.21 trillion. With parallel increases in auto loans and student debt, it’s easy to see how millions of households are struggling financially.

While debt is often viewed as the primary issue, it’s really just a symptom of a deeper problem—financial illiteracy. Many people turn to credit not because they want to, but because they haven’t been equipped with the knowledge or tools to manage their money differently. That’s why addressing debt without tackling financial literacy is like treating a fever without addressing the underlying infection. The real solution lies in fostering financial education and adopting a structured approach to money management, like the 7 Money Milestones.

Why Rising Debt Signals a Bigger Problem

It’s important to understand that not all debt is inherently bad. Loans can help people achieve important goals, like buying a home or starting a business. But when debt is used to bridge the gap between income and everyday expenses—or worse, to cover emergencies—it becomes a sign of financial instability.

Why do so many people fall into unhealthy debt patterns? The answer lies in a troubling lack of basic financial education. Many aren’t taught how to budget, save, or prepare for the unexpected. Without these skills, they turn to credit cards or personal loans, often underestimating the long-term impact of high-interest rates.

This financial illiteracy isn’t just an individual problem; it ripples through families and communities. Over time, it traps people in cycles of debt that become harder to escape from.

The Financial Impact of Poor Money Management

1. Living from One Emergency to the Next

Without proper planning, unexpected events—like car repairs or medical expenses—can become financial crises. Many households don’t have the savings to buffer these shocks, leading them to rely on credit. But credit card interest rates often exceed 20%, turning even modest debt into a long-term burden.

2. Falling Behind on Payments

The report shows a slight rise in delinquency rates, with 3.6% of debt balances now overdue by 90 days or more. For many, missed payments are not the root problem but the result of poor cash flow, lack of savings, and reliance on credit to begin with.

3. Economic Ripple Effects

On a larger scale, high household debt weakens the broader economy. When people spend more on interest and repayments, they cut back on necessary goods and services, reducing consumer spending. This can lead to broader economic slowdowns, tighter lending, and less job security—all of which exacerbate household debt levels even further.

Understanding the Debt Cycle—and How to Break It

The cycle of debt often starts with a single financial misstep or unexpected event. Without savings or a clear plan, people take on high-interest debt to cover immediate costs. Over time, interest payments pile up, making it harder to save or pay off balances. And without seeking financial education, people often repeat the same mistakes, keeping them trapped in a cycle that feels impossible to escape.

But this cycle can be broken. The key lies in addressing the root cause—financial illiteracy—and taking proactive steps toward financial stability. That’s where the 7 Money Milestones come in as a critical framework.

Why the 7 Money Milestones Are the Best Solution

The 7 Money Milestones offer more than just a way to manage money—they provide a strategy to address financial illiteracy, helping people make informed decisions, avoid debt, and achieve long-term stability. Each milestone tackles a critical aspect of financial health, building a solid foundation that makes debt reliance unnecessary.

1. Get a Financial Education

The first step to breaking free from the debt cycle is understanding how money works. Learning about budgeting, interest rates, and credit management empowers you to make smarter financial choices.

For instance, instead of relying on a high-interest payday loan, someone with financial education could identify alternatives like negotiating payments with creditors or accessing community resources. You don’t need formal training—online courses, podcasts, and financial advisors are great places to start.

2. Secure Proper Protection

Financial emergencies are inevitable. Without insurance, unexpected medical bills or accidents can derail even the best budget. Protection through life, health, and disability insurance can prevent financial devastation and reduce reliance on high-interest debt during crises.

Think of it as creating a shield for your financial future. When emergencies arise, you’ll have a plan in place that protects you and your loved ones without adding to your debt burden.

3. Create an Emergency Fund

One of the key reasons people fall into debt is the lack of an emergency fund. By saving three to six months’ worth of expenses, you can cover unexpected costs without resorting to credit.

Even small, consistent contributions—like setting aside $50 per paycheck—can grow into a meaningful safety net. This fund is vital for staying afloat during life’s inevitable curveballs, from job loss to surprise medical bills.

4. Apply Debt Management

For those who are already in debt, managing it effectively is crucial. The debt snowball (paying off small balances first) or debt avalanche (tackling high-interest debt first) methods work well.

This milestone isn’t just about reducing what you owe—it’s about freeing up cash flow and eliminating the financial stress that comes with heavy debt burdens.

5. Increase Cash Flow

Increasing your income while keeping expenses under control is a game-changer. Whether it’s picking up a side hustle, requesting a raise, or cutting back on unnecessary spending, improving your cash flow gives you more flexibility to save and invest.

For example, cutting out an unused subscription could save $15 a month. Over time, that small effort adds up, giving you extra funds to pay off debt or build wealth.

6. Build Your Wealth

Once debt is under control, it’s time to think long-term. Investing in a retirement plan, building a diversified portfolio, or contributing to tax-advantaged accounts like an IRA can help you grow your wealth.

The earlier you start, the greater your wealth grows thanks to compound interest. Even modest investments can create significant returns over time and help you retire comfortably.

7. Protect Your Wealth

Finally, wealth protection ensures that all your hard work doesn’t go to waste. Estate planning tools, like wills and trusts, safeguard your assets and prepare for generational wealth transfer. Regularly reviewing your insurance plans also ensures you’re protected against life’s uncertainties.

This milestone secures financial freedom not just for you, but for future generations.

How Financial Professionals Can Help

Breaking free from debt and tackling the 7 Money Milestones can feel overwhelming. That’s where connecting with a financial professional can make all the difference. They can help assess your situation, create customized action plans, and provide accountability as you work toward your goals.

A professional can do more than show you where you’re overspending—they provide a roadmap to financial health, recommend the best investment strategies, and help you protect your wealth.

A Roadmap to Financial Freedom

Debt doesn’t have to be a lifelong burden. By addressing financial illiteracy with the 7 Money Milestones, you can break the debt cycle, rebuild financial stability, and create a blueprint for lasting wealth.

It all starts with education and small, strategic actions. Take the first step today—your financial future depends on it!

Financial Literacy and Its Impact on Black America

Black History Month provides a crucial opportunity not only to celebrate the achievements of Black Americans but also to examine the challenges that continue to shape their economic and social reality. While strides have been made, economic imbalance persist, from a widening wealth gap to barriers in employment and homeownership. Financial literacy—understanding and effectively using financial skills—emerges as a vital tool in bridging these gaps, empowering individuals and communities to break cycles of financial insecurity.

Understanding the Economic Challenges

To understand the importance of financial literacy, it's essential to first acknowledge the economic state of Black America today. Despite progress over decades, notable hurdles remain, as highlighted in the data from the report "The economic state of Black America" Below are some key issues:

1. The Wealth Gap

One of the most glaring disparities is the racial wealth gap. Black Americans, who make up over 12% of the U.S. population, own just 3.4% of the nation's wealth. This share has decreased sharply from 4.7% in 2017. By contrast, white Americans, who make up 62% of the population, control 84% of the nation’s wealth.

As a whole, Black Americans have more wealth than ever, totaling $5.4 trillion. However, their share of the total wealth pool remains alarmingly small and continues to shrink. This lack of wealth accumulation limits opportunities for generational progress.

2. The Homeownership Divide

Homeownership is one of the primary ways Americans build and transfer wealth across generations. However, Black households consistently face a huge gap in homeownership rates. Data from the last two decades reveals that this gap remains largely unchanged, limiting many in the Black community from benefiting from property ownership and equity gains.

3. The Employment and Unemployment Gap

While the unemployment gap between Black and white Americans has narrowed in recent decades, Black unemployment rates are still consistently higher. Additionally, regional disparities worsen the problem. For instance, states like Kentucky show far greater racial barriers in the workforce compared to others like Maryland.

4. Limited Access to Banking

Banking access remains a significant barrier. Approximately 10.6% of Black households are unbanked, which is the highest rate among all racial and ethnic groups. Many rely on alternative services like check-cashing businesses, which come with higher fees and fewer protections, limiting their ability to save securely or access credit at fair rates.

5. Educational and Business Disparities

Black Americans continue to face challenges in education and business ownership. While the rate of Black-owned businesses has grown by 57% over five years, these businesses still represent only 3.31% of all U.S. businesses. Likewise, while Black students consistently earn around 10% of bachelor’s degrees, this share has not grown significantly, lagging behind increases seen in other minority groups.

These challenges underline the importance of financial literacy in building resilience and generating broader economic opportunities for the Black community.

The Role of Financial Literacy

Financial literacy is not a cure-all, but it is a powerful way to empower individuals to make informed decisions about their money. At its core, financial literacy teaches fundamental skills such as budgeting, saving, investing, managing debt, and understanding credit. For Black communities facing unique economic barriers, these skills can be life-changing. Here’s why financial literacy matters and how it can address some of the challenges outlined above:

Closing the Wealth Gap

The wealth gap often stems from historical exclusionary practices like redlining and unequal access to education and credit. Financial literacy equips individuals to make strategic choices about wealth building, such as investing in stocks and mutual funds. According to the report, Black Americans saw a modest 3.4% growth in stock ownership from 2017 to 2024. With more education on how the stock market works and how to start investing, this figure could rise substantially, encouraging wealth accumulation.

Similarly, financial literacy programs, like our 7 Money Milestones, that focus on teaching about the power of compound interest, proper protection, retirement plans, and estate planning, can lead to more long-term financial stability.

Expanding Homeownership

For many, buying a home remains intimidating, especially when navigating mortgage applications or dealing with credit scores. Financial literacy can demystify the process, providing individuals with tools to improve their creditworthiness, understand down payment assistance programs, and find loans with reasonable rates. By spreading knowledge about these resources, more Black families can access the housing market and begin building intergenerational wealth.

Tackling Employment Barriers and Budgeting

High unemployment rates make it difficult for many households to cover even basic expenses or set aside savings. Financial literacy can help families better manage their resources by teaching budgeting and disciplined spending practices. For example, a family struggling with high medical debt—disproportionately common among Black households—might learn to renegotiate bills or consolidate debt after engaging with a literacy program.

Increasing Banking Access

Financial literacy also plays a significant role in reducing the unbanked rate. By educating individuals about the benefits of opening savings and checking accounts, communities can work towards transitioning from costly alternative financial services to traditional banking. Programs that partner with community credit unions or nonprofits could further this goal by reducing barriers like distrust of banks or lack of information.

Encouraging Entrepreneurship and Higher Education

Black-owned businesses already grow at a rate surpassing general business growth, with a 57% increase over five years. But financial struggles hinder many budding entrepreneurs from scaling their operations or accessing capital. Financial literacy education tailored to aspiring business owners could include topics like writing grant proposals, navigating small business loans, or even crowdfunding strategies.

Similarly, programs aimed at high school and college students could highlight ways to reduce debt while pursuing higher education, such as applying for scholarships and grants or considering strategies to handle student loans.

Actionable Steps to Improve Financial Literacy

Implementing widespread financial literacy is no small task. However, there are many practical steps that individuals and organizations can take to accelerate change. Here are some actionable solutions:

1. Community-Based Financial Literacy Programs

Hosting free workshops or seminars in community centers, schools, and churches can make financial education more accessible. For example, our 7 Money Milestones covers topics like budgeting basics, understanding retirement accounts, and debt management, which could empower families to take control of their finances.

2. Partnering with Schools

Integrating personal finance education into school programs ensures that future generations grow up equipped to handle their money. Programs could include lessons on saving, balancing a budget, and understanding credit.

3. Leveraging Technology

Apps that offer financial literacy tools and resources provide a practical way for individuals to learn on their own. For example, platforms like budgeting apps or websites offering free financial courses could bridge the knowledge gap.

4. Supporting Black Financial Professionals

Representation matters. Increasing the visibility of Black financial professionals, or providing mentorship programs for young people interested in financial careers, could inspire others in the community to seek guidance from those who understand their lived experience.

5. Learning from Existing Success Stories

Highlight success stories of individuals or communities that have transformed their economic realities through financial literacy. These narratives can inspire others to pursue their own paths of empowerment.

A Path Forward

While the barriers facing Black America are vast, financial literacy provides a pathway toward empowerment. Whether it’s helping families save for their first home, guiding students through higher education affordability, or inspiring entrepreneurs to grow their businesses, the ripple effects of increased financial literacy are profound.

This Black History Month, we are reminded of the resilience and strength of Black communities in navigating centuries of economic inequity. By championing financial literacy as a tool for change, we honor that legacy—and help build a future defined by abundant opportunity, economic stability, and generational wealth.

- Jana B. Woodhouse, Certified Financial Educator®

Gen Z’s New Blueprint for Retirement

Balancing Flexibility with Knowledge Is Key to Their Success

For many, retirement represents the ultimate goal—a golden phase of life when work slows down, and you enjoy the fruits of decades of savings. But for Generation Z, born after 1996, this classic ideal of retirement feels outdated. They’re crafting their own financial paths, characterized more by flexibility and immediate goals than by distant horizons.

Yet, as promising and adaptable as their approaches might be, Gen Z faces significant challenges. The 2024 TIAA Institute study, “From Gap Years to Golden Years,” reveals critical insights into their financial habits, their relationship with retirement, and the unique position they’re in to succeed—if they’re given the tools and guidance they need.

Who is Gen Z?

To begin, it’s essential to understand what shapes Generation Z. They are the most diverse and educated generation in U.S. history, making up 20% of the population. Raised during defining global events such as 9/11, the Great Recession of 2008, and the Covid-19 pandemic, they’ve developed a blend of technological savvy and social awareness that sets them apart.

This is a generation accustomed to instant access to information, but they’ve also entered adulthood under financial pressure. With rising inflation, immense housing costs, and student loan burdens, many of them are focused on surviving the present rather than planning for the future.

Gen Z’s Mixed Approach to Saving

Financial literacy might be more important to Gen Z than any other generation before them simply because they face unique economic conditions. The study highlights a surprising discrepancy within their savings habits. While 84% of Gen Zers save money monthly, their approach leans heavily toward liquidity.

52% rely exclusively on traditional savings accounts to set aside funds, while only 17% invest through after-tax brokerage accounts or retirement-focused investments. When it comes to long-term goals like retirement, the number of committed savers dwindles—only 20% of Gen Zers are actively saving for their golden years. This limited focus on long-term growth can leave them vulnerable as they age, especially given looming concerns over the future of Social Security.

The primary reason for their hesitancy boils down to a knowledge gap. For 35% of those surveyed, a “lack of knowledge about where to start” was the top reason for not saving for retirement. This highlights a critical need for greater education on the importance of long-term investments.

Prioritizing Short-Term Goals Over Long-Term Stability

Unlike older generations, Gen Z has a different set of priorities. Instead of setting money aside for retirement or emergencies, they prefer to focus on immediate ambitions like housing and travel. According to the study, 19% save primarily for travel, 18% for transportation, and 17% for housing costs—all expenses tied to their goals of personal independence and self-expression.

These priorities are understandable given the generational challenge of affording basic needs. For example, Gen Z spends an average of 51% of their monthly budget on housing, which is a significantly higher portion compared to older generations. Planning for something as distant as retirement can feel impossible when they’re already stretching their income to make ends meet.

While this focus on the “now” reflects thoughtful living in the moment, the long-term costs could be enormous. A lack of robust retirement savings leaves Gen Z unprepared for potential hardships, including healthcare needs and rising living costs later in life.

Liquidity and Flexibility

What defines Gen Z’s financial approach is their obsession with flexibility. Saving through liquid options, such as basic savings accounts, gives them more control. This flexibility aligns with their vision of achieving financial freedom rather than focusing solely on traditional retirement.

The TIAA study notes that one in five Gen Zers doesn’t expect to retire at all. Instead, they imagine a future that includes working less, pursuing passion projects, or taking multiple career breaks. Saving money becomes less about an end goal and more about enabling this flexible lifestyle.

Part of this emphasis on liquidity stems from a broader mistrust of traditional financial systems. Platforms like Robinhood and Acorns have gained traction among younger investors because they prioritize accessibility and cultural relevance, catering to this generation’s desire for simplicity and control. However, this same mindset often makes Gen Zers hesitant to fully commit to long-term investment vehicles like 401(k)s. Much of this reluctance can be traced back to a lack of understanding about how these plans work and the substantial benefits they offer, such as employer matches, tax advantages, and compound growth.

Employers Step Up

Despite their reservations, employer-sponsored 401(k) plans have proven to be a major stepping stone into retirement savings for many Gen Zers. According to the study, 66% of those saving for retirement do so through these plans. Features like automatic enrollment and employer matching contributions make 401(k)s an accessible and appealing option, helping bridge the gap between Gen Z's need for liquidity and their long-term financial goals. These programs showcase the potential of traditional systems when adapted to meet the needs of a modern, cautious, and tech-savvy generation.

However, access to these benefits isn’t universal. Black and Hispanic employees are disproportionately less likely to have access to employer-sponsored retirement plans, deepening equity gaps that leave many workers behind. Employers who expand such programs and include educational tools can help young employees take meaningful steps toward securing their financial futures.

A Deficiency in Financial Literacy

The greatest obstacle to Gen Z’s financial success may not be external pressures like inflation or housing costs. Rather, it’s their lack of financial knowledge. According to the study, while 57% of Gen Z respondents believe they make good investment decisions, only 37% were able to correctly answer financial literacy questions.

Gen Z’s confidence in their financial decision-making often masks a deeper challenge—navigating the overwhelming sea of advice available online. Growing up in the technology era, they’ve mastered the art of finding information at their fingertips. But the real difficulty lies in interpreting whether that advice applies to their unique situations. Without proper guidance, many find themselves stuck in a loop of uncertainty, thinking, “I’ll figure this out later.” This inaction, spurred by conflicting advice from online “finfluencers” (financial influencers) and unreliable sources, limits their financial growth.

Further complicating matters, 61% of Gen Zers rely on their parents for financial guidance, which, although helpful, can perpetuate outdated perspectives if the parents themselves lack financial expertise.

Even with seemingly endless online resources, Gen Z could benefit from structured education. 90% of U.S. adults believe personal finance should be taught in high school, according to the National Endowment for Financial Education. Teaching these skills early could bridge the knowledge gap and better prepare young adults for long-term financial success.

Why Professional Guidance Matters

Professional financial guidance could be the game-changer Gen Z needs to secure a stable future. Financial professionals bring more than just expertise—they offer clarity in an overwhelming landscape of generic online advice. By tailoring strategies to fit individual situations, they empower young adults to take control of their financial decisions now rather than postponing essential plans for the future.

For instance, professionals can show Gen Z how to invest without sacrificing liquidity, maximizing opportunities while staying flexible. They can help young workers unlock the full potential of employer benefits, like 401(k) matches, and unravel complex concepts such as healthcare costs, tax-advantaged accounts, and compound interest. These personalized insights turn daunting ideas into manageable steps.

Crucially, this guidance must align with Gen Z’s values and lifestyle. When financial strategies are framed around goals like achieving freedom to travel, pursuing passion projects, or reinventing careers, planning becomes not just practical but inspiring. By connecting long-term saving to the life they want to build, financial professionals can make the process relatable, actionable—and deeply motivating.

Meeting Gen Z Where They Are

To truly support Gen Z, educators, employers, and policymakers must meet them where they are. This generation isn’t opposed to financial planning—they simply need tools that reflect their priorities and help ease their financial anxieties.

Key steps include:

- Financial Literacy Education: Introduce engaging, relatable finance courses into high schools and colleges to equip young adults with practical knowledge.

- Customized Savings Tools: Develop financial products that balance liquidity with long-term growth, allowing Gen Z to feel confident in their investment choices.

- Accessible Employer Programs: Expand retirement plans and offer greater 401(k) matches, especially for underserved communities, to level the playing field.

- Supportive Messaging: Reframe retirement not as a fixed point of life but as a chapter that enables freedom, professional breaks, and a sense of security.

The Road Ahead

Gen Z has the potential to achieve financial success, but they can’t get there on their own. With knowledge gaps holding many back and current systems tailored to older generations, this group needs additional support to thrive. By expanding access to financial literacy and offering professional guidance, we can help Gen Zers not only prepare for retirement but also create the flexible, fulfilling lifestyles they aspire to. And in doing so, we foster more equitable systems that benefit everyone. The future of Gen Z depends on education, accessibility, and adaptability. Armed with these tools, they’ll not only succeed—they’ll redefine what success looks like.

- Lauren Mathews Fairey and Christa Mathews

Co-authors of "HowMoneyWorks for the Next Generation: Act Now or Pay Later"

How to Plan for an Unexpected Retirement

Many of us envision a future where we retire when the time feels right, stepping away from work with a well-prepared financial cushion and years of enjoyment ahead. But in reality, life rarely sticks to the script. According to the Transamerica Center for Retirement Studies, 58% of Americans retire earlier than they planned, often due to unanticipated events. From health issues to job layoffs, unexpected retirement is more common than people think—and it can leave you scrambling to adjust to a new reality.

The good news? With some proactive planning and smart strategies, you can protect yourself financially and emotionally against the curveballs that may come your way. Whether you’re years away from leaving the workforce or already thinking about retirement, here’s how to prepare for the possibility of retiring earlier than planned.

Why Do People Retire Earlier Than Expected?

Before understanding how to plan for an unexpected retirement, it’s essential to consider why so many people face this situation in the first place. While everyone’s story is different, there are common factors that cause early exits from the workforce.

Health Challenges

Health-related issues are the leading reason behind early retirement—cited by 46% of those who retire prematurely. Whether it’s managing a chronic illness, recovering from a major medical event, or experiencing physical limitations from aging, personal health can derail even the most carefully outlined retirement plans.

Job Loss or Workplace Issues

A close second is employment-related challenges, which account for 43% of early retirements. Sometimes, the decision to retire isn’t yours to make—layoffs, company buyouts, or organizational restructuring can push workers out unexpectedly. Even age-related biases at work, no matter how subtle, can create circumstances that hasten retirement.

Family Responsibilities

For 20% of early retirees, the need to care for a loved one is the main driver. This is especially common among women, who often take on the role of caregiver for aging parents, a spouse, or children. These family commitments can make it hard to juggle a job while meeting caregiving demands, leading to a decision to leave the workforce sooner than expected.

The Financial Challenges of Unexpected Retirement

Retiring earlier than anticipated comes with its own set of financial hurdles. The biggest challenge? Less time to save and the need to stretch existing retirement savings over more years.

Lost Earning Potential

With fewer productive years in the workforce, early retirees miss the opportunity to maximize earnings, invest more, and boost their savings accounts. It’s even more daunting when you consider the reduction in potential Social Security benefits—taking payments before reaching full retirement age can reduce your monthly checks by 30% or more.

Extended Retirement Years

If you plan to live well into your 80s or 90s, an earlier-than-expected retirement means stretching your resources even further. That’s less time for your nest egg to grow and more years relying on what you’ve built.

Unplanned Expenses

Not all expenses in retirement are predictable. Health care costs, in particular, often rise sharply as we age—and retiring prematurely can mean losing employer-sponsored health insurance. On top of that, unforeseen family needs or caregiving responsibilities can quickly drain financial reserves.

How to Prepare for an Unexpected Retirement

Though unexpected retirement poses financial and emotional challenges, careful planning gives you the tools to adapt and thrive. Here are proven strategies to help you prepare for the unexpected.

1. Save Early and Save Often

The single most important thing you can do to safeguard your financial future is to save as much as possible while you’re working. Start now, even if you can only set aside a small amount. Over time, consistent contributions to a 401(k), IRA, or similar retirement account can grow significantly, thanks to compounding interest.

If you already have a retirement savings plan, consider upping your contributions by a percentage or two. These small adjustments may not feel significant today, but they can mean tens of thousands—or even hundreds of thousands—more in retirement savings over the long term.

2. Reduce Fixed Expenses

Reducing your cost of living today not only frees up money to save for retirement but also prepares you to live within a leaner budget if you retire early. Focus on repaying any outstanding debt, like credit cards, car loans, or even your mortgage.

Lowering fixed expenses such as housing costs, transportation, and utilities also provides financial breathing room. Try negotiating lower rates on recurring bills or adopt more frugal spending habits. The less you owe, the longer you can stretch your savings in retirement.

3. Plan for Health Care Costs

Health care is often the most unpredictable expense in retirement, especially if you need to retire earlier than expected and lose workplace coverage. To prepare, look into supplemental health insurance options or start an HSA (Health Savings Account) if you qualify. This tax-advantaged account lets you save for medical expenses now and in the future.

Consider enrolling early in a private health insurance plan, which might be more affordable than relying on emergency options in retirement. Remember, Medicare doesn’t kick in until age 65—so planning for those “in-between” years is key.

4. Have Honest Caregiving Conversations

For those concerned about caregiving responsibilities, open communication can reduce future stress and financial strain. Talk to your family about expectations, roles, and resources for caregiving well before the need arises.

If you’re caring for aging parents, consider whether they’ve planned financially for their own care. If not, discuss potential solutions together—like long-term care insurance, downsizing their home, or tapping into community services. Proactive planning for caregiving ensures you aren’t left facing sudden financial surprises.

5. Create an Alternate Financial Timeline

While your ideal retirement timeline may involve working until 65 or older, it’s crucial to plan for “what if” scenarios. Ask yourself questions like these when developing a financial contingency plan:

- If I had to retire at 62 instead of 65, would I have enough savings to cover the gap?

- If my income were cut short, how would I adjust my budget?

- How can I map out early withdrawal strategies for Social Security benefits without drastic reductions?

Working through these alternate scenarios with a financial professional—or even using retirement planning tools online—allows you to make informed decisions and avoid panicking later.

6. Stay Flexible

Flexibility is a key ingredient in weathering unexpected retirement. Laws, Social Security policies, and economic landscapes change over time, so staying adaptable ensures you’re prepared for whatever comes your way.

Diversify your retirement savings by contributing to multiple accounts (like a combination of traditional IRAs, Roth IRAs, and taxable savings). This gives you multiple options for withdrawing funds under different tax scenarios.

On a personal level, reassess your goals, budget, and retirement plan every year. Life is full of surprises, and frequent check-ins ensure your plans align with your current reality.

7. Seek Professional Guidance

Finally, consulting with a financial professional is one of the most effective ways to prepare for an uncertain retirement future. A skilled professional can help you outline scenarios, calculate your savings needs, and explore investment strategies tailored to your goals. Their expertise can uncover risks you might not have considered and guide you toward a more secure future.

Bright Spots Amid the Challenges

Feeling nervous about retiring early? Take comfort in the broader picture. According to Transamerica’s survey, 89% of retirees report being generally happy—and 86% say they’re enjoying life. This proves that even if retirement doesn’t go exactly as planned, it can still bring joy and fulfillment.

With clear planning, thoughtful adjustments, and a resilient spirit, you can successfully ensure financial stability and peace of mind—whether retirement begins at 55, 65, or any unexpected time in between.

Start today, and be ready for whatever the future holds.

Navigating January After a Holiday Spending Hangover

The holiday season often pulls at our heartstrings—and our purse strings. It’s a magical time filled with joy, togetherness, and splurging on gifts, decorations, and festive outings. However, when the sparkle fades and the calendar flips to January, many of us are left confronting the aftermath of holiday indulgence. If you’ve gone overboard on spending and are now staring at a pile of credit card bills, you’re not alone. According to a recent survey, the average American racks up over $1,000 in holiday debt. But what happens now, and how can you regain control?

Let us explores the real consequences of unchecked holiday spending and offers practical, tailored solutions to help you get out of debt and ensure that history doesn’t repeat itself next December.

The Consequences of Losing Control During the Holidays

1. Mounting Credit Card Debt

The joy of gift-giving often comes at a steep cost. A report indicates that most Americans lean heavily on credit cards to fund their holiday spending. By the end of the festive season, the average holiday debt exceeds $1,000. For households already carrying significant balances—averaging nearly $7,000 month-to-month—this additional burden can feel insurmountable. If holiday debt is left unchecked, it gets compounded by interest, with many paying hundreds (even thousands) in charges over time.

For instance, consider someone who charged $1,230 to their credit card with an average interest rate of 16.5%. If they can only afford minimum payments of $30 a month, it would take over five years to pay off the balance, with around $592 in added interest. Simply put, holiday cheer comes with a long financial hangover for many Americans.

2. Struggling to Pay it Off

While good intentions may suggest otherwise, most shoppers don’t repay their holiday spending quickly. Only 42% of people plan to eliminate their debt within three months. On the flip side, nearly a quarter admit that they’ll make only the minimum payments, stretching out repayments over years. This delay not only deepens financial stress but also diminishes the ability to achieve other financial goals like saving for emergencies, investing, or even splurging on future holidays.

3. Rising Interest Costs

Adding salt to the wound, rising interest rates on credit cards make it even harder for those struggling with holiday debt. Recent interest rate hikes by the Federal Reserve mean consumers now face an additional $1.6 billion annually in credit card finance charges. This rising expense makes January an especially steep uphill climb for shoppers who overspent the previous year.

4. Psychological Stress

Beyond numbers and interest rates, there’s the emotional toll. Guilt, regret, and anxiety are common companions for those confronting holiday overspending. Seeing inflated balances and processing mounting obligations can quickly erode one’s mental well-being. Such stress might even lead to avoidance behaviors, like ignoring bills or skipping payments altogether, which only worsens the spiral.

Steps to Take in January

Now that the problem is laid out, January is the ultimate chance to turn things around. While the situation may seem daunting, the good news is that effective planning and decisive action now can not only tackle holiday debt but also build a more financially secure future.

1. Understand Your Current Financial Reality

Before you can make progress, you need clarity. Start by gathering and reviewing all financial statements, including credit card bills, bank accounts, and any other debts. Ask yourself:

- How much did I spend during the holidays?

- What is the total amount owed across all debts, including interest rates?

- Are there upcoming expenses this month that need prioritization?

A clear picture of your financial standing allows you to set realistic goals and create an action plan.

2. Create or Revise a Budget

If you don’t already have a monthly budget, now is the time to make one. If you do, revise it to account for prioritized debt repayment. A simple budget includes categories for income, essential expenses (like rent, utilities, and groceries), discretionary spending, and debt payments. Here’s how to make every dollar count this month and beyond:

- Reduce unnecessary spending by cutting back on eating out, subscriptions, and nonessential shopping.

- Funnel these savings directly into your debt repayment fund.

- Aim to live below your means to free up extra cash.

3. Prioritize Your Payments

Not all debts are equal. Focus on paying down high-interest credit card balances first to minimize the long-term cost of borrowing. You might choose one of these repayment strategies depending on your financial personality and motivation level:

- Debt Snowball: Pay off your smallest debt balance first while making minimum payments on the rest. Gradual, early wins will keep you motivated.

- Debt Avalanche: Concentrate on paying off debts with the highest interest rates first, which saves the most money over time.

For extra efficiency, consider consolidating debt into a lower-interest loan or transferring balances to a credit card with a 0% introductory APR offer.

4. Seek Financial Support

If your debt situation feels overwhelming, you don’t have to face it alone. Reach out to a financial professional, credit counselor, or local nonprofit organization for guidance. Many resources, including free consultations, are designed to help individuals create plans to tackle debt and build healthier financial habits.

Alternatively, you may contact creditors directly to negotiate interest rates or request payment plans. Some credit card companies allow hardship applications, which can lead to temporarily lowered interest rates.

5. Look for Side Hustles

Sometimes cutting expenses isn’t enough. If possible, consider adding a side hustle, such as freelancing, tutoring, babysitting, or selling unused items online. Even small amounts of extra income can make a big impact when dedicated solely to debt repayment.

6. Automate Payments and Savings

Setting up automatic payment systems removes the temptation to skip a bill or reduce the repayment amount. It’s also a helpful way to ensure punctuality and protect your credit score. Better yet, automate a small monthly savings deposit, no matter how tight your budget feels. Over time, this creates a financial cushion to prevent future holiday debt.

Avoiding Future Holiday Spending Traps

Addressing today’s debt is only half the battle. Preventing another spending overload at the end of this year calls for thoughtful preparation. Take these steps well before the holidays roll around again:

1. Plan a Holiday Budget in Advance

Avoid overspending by setting a realistic holiday budget for gifts, décor, and festivities. Challenge yourself to keep all spending within a specific dollar amount. Tuck away money each month into a dedicated holiday savings account so you're better prepared once December arrives.

2. Adopt Gifting Alternatives

Rather than piling on expensive bought items, explore alternatives that hold meaning without breaking the bank. Some ideas include handmade gifts, sentimental tokens, or a baked good basket for family and friends. Additionally, organizing Secret Santa exchanges reduces the financial stress of buying for an entire group.

3. Shop Smart

Be strategic by shopping sales, comparing prices online, and searching for discount codes. Purchasing gifts throughout the year—when deals arise—can spread costs and eliminate the December rush.

4. Reflect on Last Year’s Lessons

This January is the perfect time to assess what went wrong in your spending habits. Were you lured by sales? Did you say “yes” too often to group activities or parties? Identify the triggers and plan alternative approaches to avoid them this year.

A Brighter Financial Future

Holiday debt can feel overwhelming, but it’s also an opportunity to evaluate and adjust your financial habits. By facing the problem head-on in January, you stand a better chance of reducing your debt quickly and painlessly. Use practical budgeting tools, prioritize repayment, and lean on support systems to regain control.

Ultimately, financial discipline and foresight will help you avoid repeating the same holiday spending traps next year. With these strategies in place, January doesn’t have to be the season of regret. Instead, it can be the month you lay the foundation for a healthier, stress-free relationship with money.

The Most Powerful Money Principles Every Consumer Needs to Know

The dawn of a new year brings with it a sense of renewal—a chance to reflect on the past, reset your priorities, and set goals for the future. It’s the perfect time to take control of one of the most pivotal aspects of your life: your finances. This year, why not make a resolution that has the power to transform your life? By mastering essential money principles and putting them into action, you can build a brighter, more secure financial future for yourself and your family.

It doesn’t matter where you are on your financial journey; these are the essential money principles that every consumer should understand to make smarter financial decisions, avoid common pitfalls, and build a secure financial future. By applying these principles, you can improve your overall financial health, gain better control over your spending, save effectively, and work toward your long-term financial goals.

1. Start Early, Invest Consistently

"Compound interest is the eighth wonder of the world. He who understands it, earns it; he who doesn’t, pays it.”

– Albert Einstein

Explanation: The sooner you start saving and investing, the more time your money has to grow through the power of compounding. Compounding allows the earnings on your investments to generate even more earnings over time, creating a snowball effect that accelerates your wealth. Even small, consistent contributions can lead to significant results if given enough time. Starting early not only reduces the pressure to save large amounts later but also lets your investments work harder for you, turning short-term sacrifices into long-term prosperity.

2. Live Below Your Means

"Do not save what is left after spending, but spend what is left after saving.”

– Warren Buffett